This makes me furious (From The Oxford Club)

Summary

- Earnings season is starting to wrap up as more than 75% of S&P 500 companies have reported their latest results.

- Earnings and revenue beats are in line with historical averages, but divergences beneath the surface are creating different winners and losers than 2025's market.

- These three stocks typically fly under the earnings radar in their respective industries, but their positive recent reports deserve a closer look.

Earnings season is winding down, and more than three-quarters of the companies in the S&P 500 have reported their latest results. According to FactSet, roughly 74% of firms reporting so far have beaten analysts’ EPS estimates, and 73% have beaten revenue estimates.

While these overall numbers are within the five- and ten-year averages, the dispersion between winners and losers kept the aggregate earnings growth rate flat for the period. Many of last year’s success stories have underperformed in 2026, while some laggards have posted parabolic gains. Three companies whose earnings reports don’t typically garner headlines still warrant attention for the numbers in their most recent reports. Are these one-time standouts or the sign of a larger trend?

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Click here to get the details and I'll show you how to claim your stake…

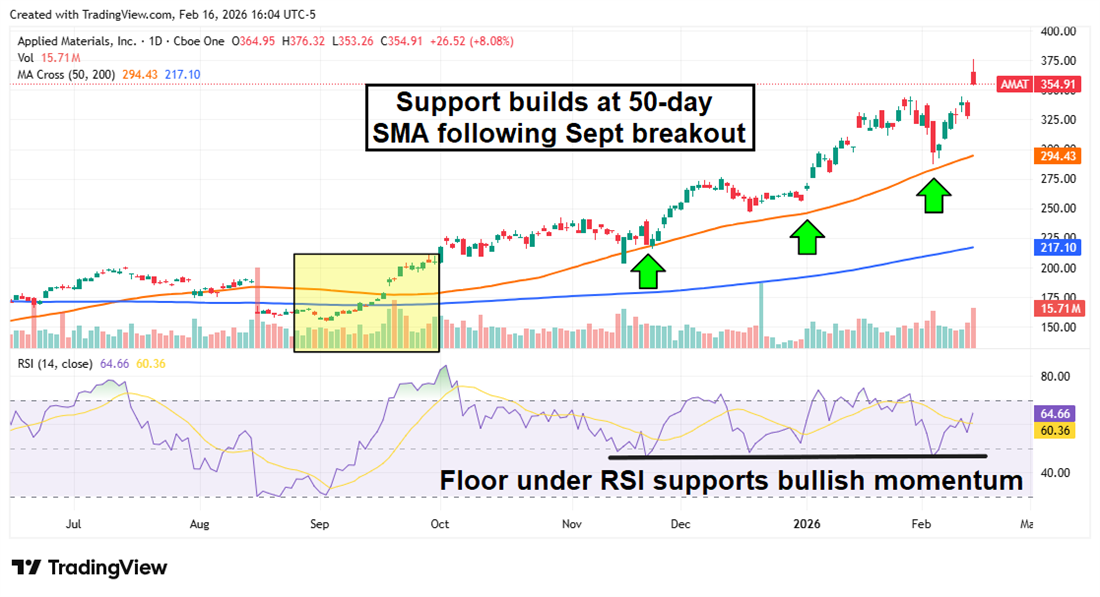

Applied Materials: Semiconductor Demand and Guidance Boost Power Double-Digit Gains

Applied Materials Inc. (NASDAQ: AMAT) is probably the most “on-the-radar” stock here, with its $280 billion market cap and $28 billion in annual sales. But as a picks-and-shovels play in the semiconductor space, Applied Materials usually reports in the background while NVIDIA Corp. (NASDAQ: NVDA) or Alphabet Inc. (NASDAQ: GOOGL) steal the headlines. However, this most recent report warrants attention as AMAT shares soared 12% following the release, driven by strong guidance and equipment demand.

The company reported its fiscal Q1 2026 results on Feb. 12 and surpassed analysts’ estimates on both EPS and revenue, with earnings beating expectations by 7%. But the news that really excited investors came on the conference call when CEO Gary Dickerson projected 20% sales growth in calendar year 2026, a figure that exceeded even the most optimistic analyst projections. Most of the company’s revenue comes from its Semiconductor Systems division, which sells flash memory, logic manufacturing equipment, transistors, DRAM, and more. Dickerson projects Q2 revenue of approximately $7.65 billion, with continued rapid growth in the Applied Global Services division.

The target price increases came in fast and furious following the optimistic report, and it received two upgrades from Hold to Buy from Summit Insights and KGI Securities. The average price target of the 17 analysts who raised the stock is now $435, representing nearly 20% upside from current levels.

AMAT shares have been in an uptrend since September, when the price crossed over the 50-day and 200-day simple moving averages (SMAs). The 50-day SMA has been a strong support level for the stock ever since, providing a bumper whenever shares dip. The Relative Strength Index (RSI) is still under the Overbought threshold of 70 despite the big earnings bump, so this rally could have staying power.

Advance Auto Parts: Turnaround Efforts Starting to Show Results

Advance Auto Parts Inc. (NYSE: AAP) may finally be returning to investablity after losing more than 50% over the last five years. The last 12 months have been particularly tumultuous for the company (and the automotive sector as a whole), as it lost more than $10 per share in Q4 2024 and then faced a wave of tariff headwinds following the Trump administration's transition. But CEO Shane O’Kelly has become relentlessly focused on cutting costs and getting “back to basics”, and these efforts are finally paying dividends.

Advance Auto Parts Q4 2025 results defied even the most generous estimates. Revenue slightly beat analyst projections ($1.97 billion vs. $1.95 billion expected), but EPS of 86 cents per share was more than double the projected figure. Same-store sales actually grew 1% over the full year, and 17 underperforming locations were closed. The 2026 guidance also boosted the stock as management projects 1-2% comps, 45% gross margins, EPS between $2.40 and $3.10, and approximately $100 million in free cash flow generation.

Some profit-taking occurred following the earnings release since the stock had already risen nearly 50% since the start of the year. However, once the dust settles, the uptrend is likely to remain in place now that the share price has burst above the 50-day and 200-day SMAs. The Moving Average Convergence Divergence (MACD) also indicates bullish activity, with the MACD line crossing above the signal line and then rising above the histogram during the breakout.

Can Amazon Solve America's Power Problem?

Amazon (AMZN) may have just cracked the AI power code and solved this country's energy problems... Jeff Bezos just doubled down on a breakthrough tech that's fast-tracking a $40 trillion industry. This is still flying under the radar, but it won't be long before this is mainstream news.

Find out how you can prepare and invest before everyone else right here.

Rivian: Narrowing Losses Lead 2026 Catalysts

Friday the 13th was anything but scary for Rivian Automotive Inc. (NASDAQ: RIVN) as the company exceeded top- and bottom-line estimates in its Q4 2025 report. YOY revenue growth actually declined 25% due to the expiration of the EV tax credits, but sales figures still beat expectations, and the company’s loss narrowed to 66 cents per share.

The smaller losses were driven by a $5,500 increase in average vehicle selling price, while the cost of vehicles sold dropped by $9,500 on average. It marked the firm's first year of gross profit, and the affordable midsize R2 model is expected to begin deliveries in Q2 2026. The company expects to sell between 62,000 and 67,000 vehicles in 2026, the low end representing a 47% increase over 2025’s total.

RIVN shares gained 20% in a volatile session following the report, although it was down from the open. The stock now sits directly at the 50-day SMA, which had previously served as a support level when shares rallied at the end of 2025. A bullish MACD cross also indicates a favorable trend, but the company will likely need a successful R2 rollout to sustain this momentum.

Read this article online ›

Stay Ahead of the Market

The best investment opportunities don't wait. Get our research and stock ideas delivered straight to your smartphone—so you never miss a market-moving opportunity. Our text alerts ensure you see timely stock ideas and professional research reports instantly, whether you're in a meeting, commuting, or away from your desk.

Get Text Alerts from American Market News (free)

No comments:

Post a Comment